Silicon Valley’s Best Kept Secret: Founder Liquidity

Ask most venture-backed founders why they get 10x more equity than employee #1, 100x more equity than employee #5, and 1000x more equity than employee #15, and you'll get the same answer: "I'M TAKING SO MUCH RISK, IT'S SO HARD TO START A COMPANY, I MADE A BIG MOVE!!!" And then you'll ask, "but why are you yelling?”

The narrative of the founder's risk is a cornerstone of Silicon Valley's mythology. Founders are celebrated for leaving stable jobs and pouring their lives into an “uncertain” and “high-risk” venture. This mythos justifies the enormous equity stakes founders hold compared to early employees who take very similar risks by joining an unproven startup.

However, there's a lesser-known aspect of the startup ecosystem that significantly shifts the risk landscape: founder liquidity.

My Experience in Early Stage Startups

Being a software engineer who has a strong preference for creativity, problem-solving, and autonomy I realized during college that very big and slow companies were not for me. I joined a startup straight out of college as employee number 8 and immediately knew I made the right choice. My skills were improving week over week, I was responsible for shipping important features and was given a lot of responsibility right out of the gate.

I eventually got pretty good at choosing strong founders to join and building great products from zero to one which in turn spawned a cycle of joining a team early, finding success, the company gets too big, and then I leave to do it again elsewhere. I have been an early or first engineer at five different companies and have had three liquidity events in a 9-year career.

The Reality of Founder Risk & Liquidity

Founder liquidity refers to the practice where founders sell a portion of their shares during a new funding round. This allows them to "take chips off the table," securing personal financial stability while continuing to build the company with a fresh influx of venture capital. This practice is often kept under wraps, discussed in closed boardrooms, and only briefly mentioned in investor updates. You would really only know this happened if you were a founder, investor, or had direct access to the cap table.

Why is it a secret that founders get liquidity in many venture rounds? Because it undermines the narrative of the founder who is "all-in." The story of the founder who mortgaged their house and lived on ramen noodles for years is compelling. It garners admiration and sympathy, attracting top talent willing to work for lower salaries in exchange for a piece of the pie. If it were widely known that founders could de-risk their financial position while their employees remained all-in, it might change how startups are perceived and valued.

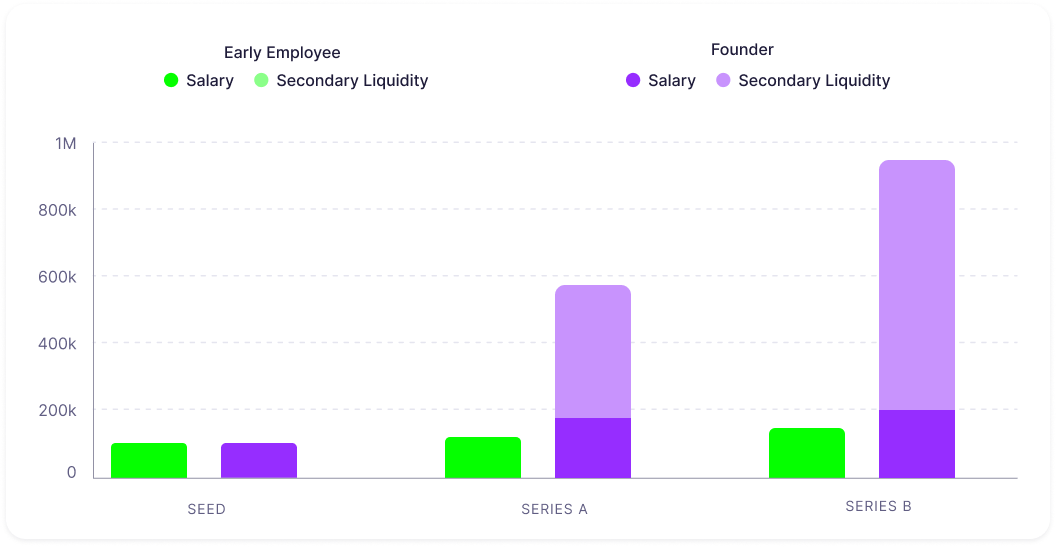

This is a graph of cash compensation over time modeled off of a real scenario that happened over 4 years. This level of founder liquidity is fairly common.

The founder in this scenario was offered $400,000 of liquidity at Series A and $750,000 at Series B and encouraged to do so by their board of investors to de-risk their own life. Liquidity was not offered to any employees and the fact that this happened at all was only revealed to people on the cap table.

Another more well-known and extreme example was in the case of Adam Neumann the founder of WeWork - Neumann was able to cash out over 2B in secondary meanwhile not a single WeWork employee was able to capitalize on their equity stakes. They were told internally how much their shares were worth at each raise, and the hype surrounding each raise continued as WeWork sky-rocketed in valuation. Neumann was smart to de-risk his position by selling as much secondary as possible during the ascent but only attempted to structure a tender offer for non-founding employees in 2019 nine years after WeWork was created. That tender offer with SoftBank fell through and employees were left with absolutely nothing. (source)

The part about these stories that feels unfair is not that the founders are getting liquidity - it's that they are the only ones getting liquidity. There are other stories like Hopin where the founder takes tens or hundreds of millions in secondary just to later sell the company for less than the liquidation preference stack and leave the employees with a grand total of zero dollars for their equity.

Right-Sizing Perception

There are a lot of odd perceptions surrounding founder liquidity:

- Investors and founders both tend to think that if employees knew founders were getting liquidity that that would negatively impact employee morale (it wouldn’t)

- Founders often feel guilty that they are getting liquidity (they shouldn’t)

- Investors think that the liquidity could taint the perception of future investors negatively (it doesn’t)

- Investors, founders, and employees all believe that founders are taking more risk than early employees (this isn’t true once founders have exclusive access to liquidity)

When I found out that my founders got access to liquidity during our series A my first thought was “That is awesome, they deserve it” my second thought was “I wonder why employees didn’t get access to any liquidity?” and then my third thought was “Is this a secret? It seems like a secret. That’s weird”. I was the only employee who knew about it because I had incidental access to the cap table.

Once I found out, I was curious if I was reading it correctly, so I immediately went to one of the founders and asked “Did you get a bit of liquidity during the series A?”. His reaction went from surprise to confusion and then he said “Yeah I did, a little bit”. I said “Wow that is awesome, congrats! It has to be nice to be able to backfill some salary after grinding for a couple of years” and he said, “Yeah, definitely.”. I could sense relief after chatting about it with him, almost like he felt better knowing that I knew about it. I never felt negative, had low morale, or anything of the sort, I trusted in my founding team and I was happy for them. If it were the case that I was lied to about it, then I would be upset and have low morale but that would be a result of being lied to - not liquidity access.

Balancing the Scales

As of 4 months ago I left a very successful stealth startup (which grew to 40M in ARR in two years) to become a founder and that is when it clicked - I expected to feel stressed, pressured, and the weight of all of the risk I was taking. What actually happened is that I realized I could have been a founder 6 years ago and I would have been taking a similar amount of risk as I did then as the first employee at tackle.io.

My intention now, as a founder, is to balance the risk for early employees by being transparent, more generous with equity, and only taking liquidity if I can also offer it to employees as well.

- Our employee option pool is 20% which is double the average

- We have a 3-month equity cliff which is 9 months sooner than the average.

- We allow employees to exercise options up to 10 years after they leave instead of 90 days.

- Our equity packages vest over 3 years instead of the industry standard 4-year period.

These changes are great, but nowhere near enough. In my view, every internal announcement of a new round at venture-backed companies should be accompanied by education and transparency around liquidity. Without transparency, none of the misperceptions have a chance of going away. The net result is that employees have a fundamentally misguided idea of the risk landscape as it shifts beneath their feet.

If you work at a venture-backed company the next time a round is announced ask if the founders took any liquidity. Do it anonymously if you have to. This question should become so common that founders and investors become transparent by default. If they say no, great - no change to risk profiles. If they say yes - great, employees are operating with the same information as the founders and investors. This levels the playing field and allows employees to assess if they are still in a lower risk bucket than the founders, or if they are now taking significantly more risk than the founders.

If employees realize they are taking more risk than the founders, maybe they'll ask for more compensation, maybe they'll congratulate the founders and move on with their day, maybe they'll start yelling: "I'M TAKING SO MUCH RISK, IT'S SO HARD TO BUILD A COMPANY, I DON'T EVEN HAVE ACCESS TO LIQUIDITY!!!". And maybe they're right.

(special thanks to anu, jessica, erika, laura, derek, and minh for reading drafts and giving feedback on this)